A Rapidly Changing Procurement Space Provides a Wealth of Opportunities

The future of procurement technology is here today.

12 min read

April 6, 2023

The process of executing a B2B transaction, or procurement, is a whale of a problem. It is much simpler for a consumer to buy one cut of cotton fabric for their sewing hobby than it is for a clothing maker to procure 1,000 pounds of cotton fabric for their shop. When businesses make large purchases, they face a gauntlet of complexities around demand forecasting, vendor discovery, price, negotiations, supply chain visibility, vendor diligence and onboarding, compliance, delivery method and timing, payment terms, payment methods, and much more.

Thankfully, solutions to this problem are evolving quickly. Procurement technology is moving towards a hub-and-spoke model in which businesses will be able to pick and choose from a “menu” of strong “point” solutions for specific steps of the process, with an orchestrator or modern intake-to-pay software at the center. This emerging system will challenge the legacy platform solutions that have dominated the space for decades.

“This is our moment,” Bain Capital’s Head of Procurement, Meghan Truchan, told me. “We procurement practitioners are up for the task of being a critical function of our companies’ short- and long-term success in the marketplace. And to do this, well-fitting technology may be our No. 1 imperative.”

The future of procurement technology is here today, and with it comes plenty of opportunities for founders.

In this piece, we’ll explore why we think the biggest opportunities are in upstream procurement, how these opportunities have grown out of the industry’s recent evolution, and where we see this growth taking the industry next.

This article includes:

I. A Massive Opportunity in Upstream Procurement

II. Waves of Procurement Technology: A Market Develops

III. The Current Wave of Innovation: Best-in-Class ‘Point’ Solutions

IV. Moving to a Hub-and-Spoke Model

A Massive Opportunity in Upstream Procurement

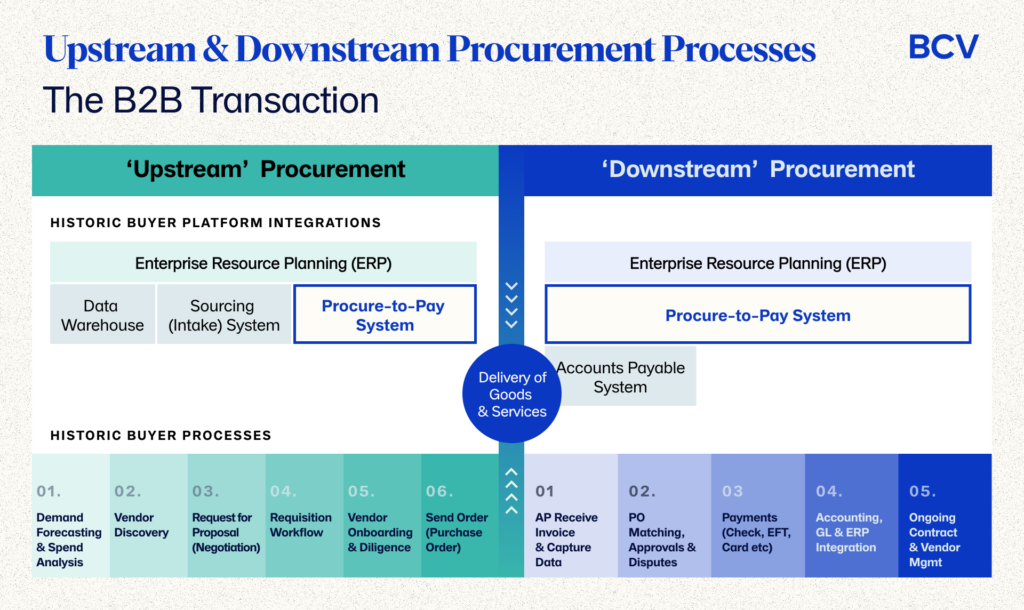

According to a February 2023 report from the San Francisco-based trade technology platform Tradeshift, 82% of B2B buyers want the same purchasing experience at work that they have when purchasing items for themselves. To better analyze why this has been so difficult to accomplish, we split procurement between “upstream” and “downstream” activities:

- Upstream activities include those before the delivery of goods and services.

- Downstream activities are those after delivery of goods and services.

Modern technology has mostly focused on solving downstream processes, but a huge opportunity exists in upstream procurement. [1]

Internal stakeholders involved in upstream procurement have historically tended to work either with legacy platform solutions such as Ariba, Coupa, or Jaggaer, or instead with an in-house set of tools (sometimes a true procurement tool, sometimes a makeshift system of Excel, Slack, email, ticketing, pen and paper, and phone). A 2021 Levvel report noted that just 39% of CPOs used any procurement solution to place orders with suppliers, while 30% and 31% did so manually and through a supplier website, respectively.

The lack of technology looks especially stark in comparison to the size of the prize in upstream procurement: Across all companies with 500+ employees globally, we estimate ~$1.1tn of wasted spend in procurement, the decisions for which are made in upstream processes. This implies billions of dollars of market cap available to cost-saving, value-providing procurement technology solutions, dependent on the levels of savings they can help generate.

Waves of Procurement Technology: A Market Develops

In the past six years, macro tailwinds and a cohort of exciting founders have driven innovation in the upstream procurement process, ushering in what we consider to be a third wave of procurement technology.

- Wave 1: The Birth of the Original Procurement Apps (1990-2000)

- The first full-suite Procure-to-Pay businesses are founded.

- Solutions include CommerceOne (1990-2004), SciQuest/Jaggaer (1995-present), Ariba (1996-present), GEP (1999-present), Ivalua (2000-present).

- Wave 2: Buy and Build Platform Strategies Create Giants (2006-2016)

- Coupa is founded in 2006 and develops a more modern Procure-to-Pay suite over the next decade through a combination of buy and build. Legacy platforms scale similarly to provide full suite offerings, enabling customer to do everything from intake to payment for goods. By 2016, legacy players are generating ~$5 billion of revenue per year.

- Major Liquidity Events: SAP acquires Ariba ($4.3 billion, April 2012); Coupa IPO ($3.4 billion, October 2016).

- Wave 3: Next-Gen Procurement Technology Companies Emerge (2017-Present)

- A small procurement revolution begins in 2017 as a record ~$960mm is raised across 71 deals (US & EU).

- These companies begin to take a different approach, focusing on building best-in-class point solutions for various parts of the procurement process instead of trying to become newer full-suite platforms.

Why Is This Proliferation of Innovation Happening Now?

Coupa’s successful October 2016 IPO generated excitement and did much to put procurement technology back on the map. The VC-backed firm based in San Mateo hasn’t slowed down since and has remained a visible example of the exciting potential of modern procurement technology.

At the same time, two other, more fundamental factors have accelerated innovation in procurement technology in recent years.

The first was an increase in the cost of everything from labor to materials, spurred by economic protectionism, tighter supply chains, the COVID-19 pandemic, and ensuing inflation. Because generating and proving cost savings is the primary goal of procurement teams, these price increases have driven them to leverage technology to source more cost-effectively.

Second, management teams have been putting growing pressure on procurement to take on strategic functions within the organization and in some cases to contribute to the business’s competitive differentiation in its market. Pushed by macro events, competitive landscapes, internal initiatives, and consumer demands, procurement teams are being asked to expand their remit and generate value beyond cost savings. They are striving to procure cheaply, quickly, flexibly, securely, sustainably, and strategically.

In response to these twin pressures, historically underserved procurement teams are turning to modern software to help alleviate pain points and improve processes. While the digitalization of procurement has been underway for some time, current tailwinds driving adoption are particularly strong.

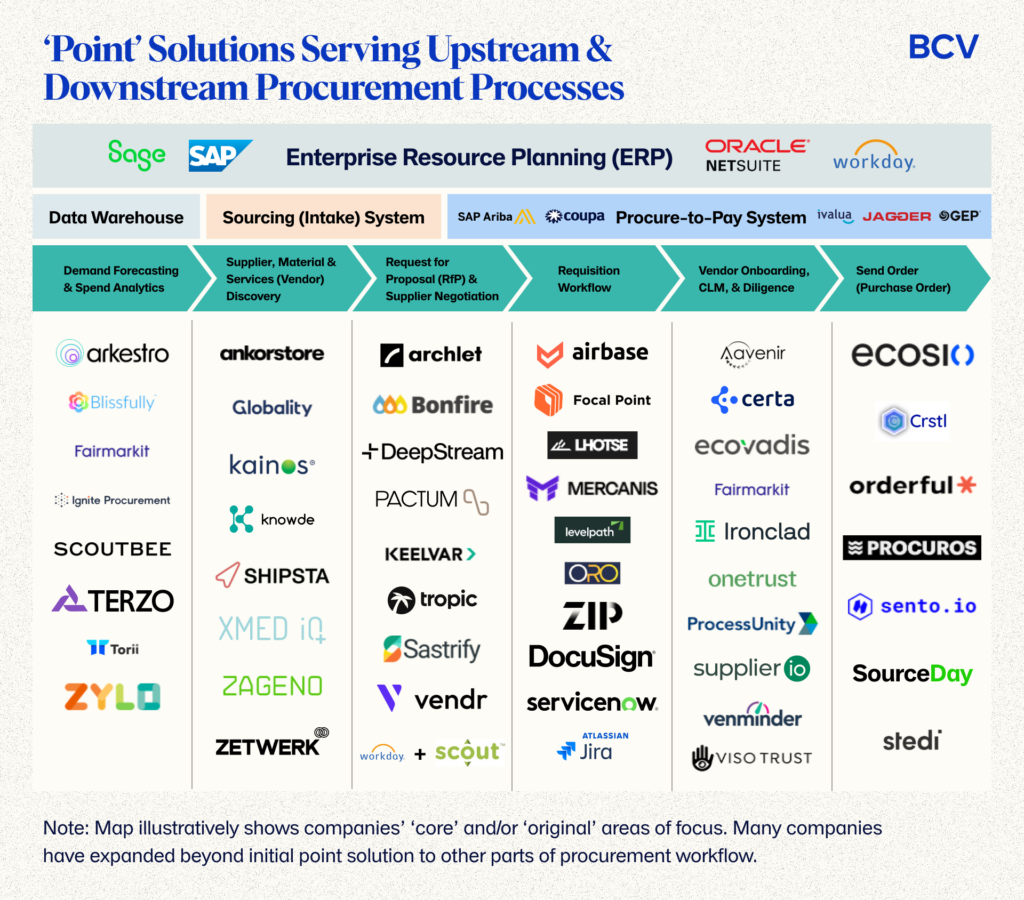

The Current Wave of Innovation: Best-in-Class ‘Point’ Solutions

To address these tailwinds, best-in-class point solutions are proliferating across the procurement workflow, from demand forecasting and vendor discovery on one end to purchase order creation and next-generation electronic data interchange (EDI) companies on the other. Each addresses a specific aspect of the procurement process. At BCV, we are excited that these point solutions are emerging to help drive value in four significant ways.

Finding External and Internal Cost Savings

A report by Bain & Company from last October noted that 60% of savings available to procurement teams should accrue via improved internal workflows, while only 40% were available through buying more cheaply. Knowing this, procurement teams are being asked to negotiate prices effectively and to strategically examine purchase specs along with the costs and potential waste of repetitive, inefficient internal workflow.

Companies are thus turning to companies like Pactum, DeepStream, Keelvar, and Sastrify to help optimize external negotiations, and Zylo, Torii, and Lightsource to focus on internal cost and time optimization.

Speeding Up and Streamlining the Purchase of Goods

Being able to buy quickly and flexibly has become an important competitive edge in periods of supply chain turmoil. Teams are therefore turning to technology to help streamline procurement, shortening times of vendor discovery, requests for proposals (RFPs) and negotiations, internal approvals, communications with vendors, and more.

Workflow software like Zip, Oro, Levelpath, and Lhotse attack the problem of inefficiently used human and software resources to speed up processes, while modern EDI companies like Orderful, Stedi, ecosio, Procuros, and Sento expedite and standardize communications with vendors.

The results are real: A Boston Consulting Group report from November noted that “bionic procurement” (tech-driven procurement) results in 2-3x faster services delivered to stakeholders.

Sourcing Quality Goods and Services

ESG (environmental, social, a governance) initiatives pushed by both consumers and regulators are making their way to procurement teams’ desks, where it is now the responsibility of procurement departments to source responsibly and transparently.

By using technology such as Ecovadis, Supplier.io, and IgniteProcurement to vet potential vendors and supply chains, procurement teams can acquire higher quality materials and services and deliver on ESG values to the organization.

Mitigating Risk in Supply Chains

Supplier risk mitigation initiatives are assigning procurement teams responsibility for the cyber, ethical, financial, and legal security of companies. This is pushing procurement teams to leverage technology to bring clarity, visibility, and structure to their buying process and protect the organization against any number of threats.

VISO Trust is a great example of a company tackling this challenge. By focusing on automating document reading and ingestion, VISO Trust provides security intelligence for clients early in the procurement process so that teams can proceed with procurement workflows assured that vendors have been vetted for cyber risk.

Moving to a Hub-and-Spoke Model

As these point solutions continue to emerge, we at BCV are excited to see how new startups and technologies grow and interact with each other.

To coordinate these solutions, we expect to see a hub-and-spoke model flourish, in which orchestration and workflow software will take a central position and connect an organization’s chosen point solution technologies.

Two major trends will drive the development of this ecosystem.

The Decentralization of Procurement

Forcing enterprise-wide usage of legacy procurement platforms has not worked well and is not how employees want to work today. More employees across the organization want to procure their own goods – whether that is the marketing group looking for third party PR consulting services, the R&D team looking for new software, or the sustainability department looking for a better source of raw materials.

As more employees turn into buyers with more technology at their fingertips and expectations for a fast, compliant, and easy way to buy things, organizations will look for best-in-class point solution tools to best equip these actors and manage their spend. Giving more autonomy for purchasing decisions means that employees will turn to specific tools to help them with their part of procurement, whether that is forecasting, discovery, negotiation, vendor onboarding, or legal compliance, along with tech review and approvals.

The Need for Increased Simplicity in an Increasingly Complex Process

Ever-present supply chain and price difficulties, alongside both the decentralization of procurement and the pressure for procurement to adopt a more strategic posture, are adding increased complexity to the buying process. Organizations are being forced to buy more strategically and flexibly, and therefore need best-in-class, purpose-built, deep tools to handle any given portion of the procurement workflow.

At the same time, as more non-professional buyers continue to enter the buying process, this complexity of content must be balanced with simplicity in experience and interface. The legacy platforms are not built to handle this. Builders of the future must aim to strike a balance between the two and to build point solutions to service these twin needs.

In response to both these trends, we believe that procurement orchestrators will continue to gain momentum and stitch together disparate people, technologies, and processes.

We have started to see the first of these develop today. Companies like Certa and Lexion have started building workflow software on top of their core initial use case: in Certa’s case Third Party Supplier Management, in Lexion’s (procurement) case, vendor onboarding. These software help connect relevant other specific solutions adjacent to their use case. Certa, for example, partners with ID verification, tax ID verification, ESG and Diversity, and Data Security software, among others, and lets users built a no-code workflow and requisition software to connect users and technology within their organization.

Others – like Zip, Oro, Levelpath, Lhotse, Paid, and Aavenir – are building something closer to pure orchestration software. With a slightly different vision but similar focus, FocalPoint aims to build a modern intake-to-procure platform. Coming from the accounts payable and expense management landscape, Airbase has recently announced that it will be the first spend management solution to work to automate the intake process for purchasing, architecting its “Guided Procurement” design as a no-code workflow orchestrator. This set is largely more focused on integrating with procurement’s major players: the canonical platforms, DocuSign and Ironclad, Jira and Asana, enterprise resource planning (ERP) firms, Slack and Microsoft Teams, and more. They may continue to add relevant, strong procurement point solutions with time.

Like their cousin point solutions, the procurement orchestrators emphasize simplicity in UI and clarity in workflow above all else, differentiating themselves from legacy platforms and helping to democratize the procurement process in the process.

We believe that this format of workflow software with point solutions has the capacity to disrupt procurement’s legacy platforms and unlock innovation. As the hub-and-spoke model takes shape in the coming years, we look forward to a new era of procurement software that delivers value across organizations, stemming from procurement’s central place in the B2B transaction.

Thank you to my partners Sarah Hinkfuss and Matt Harris for feedback and debate. If you’re excited about procurement technology, I’d love to meet you. Send me a note at pcroak@baincapital.com.

[1] Procurement innovation in AP solutions, spend management software, B2B payments companies, and next-generation logistics and delivery businesses have attracted the lion’s share of entrepreneurs and VC dollars set on improving the B2B transaction over the last 10 years. The top ten VC-backed spend management companies alone raised ~$2.5 billion and ~$1.5 billion in 2021 and 2022, respectively. In stark contrast, Maersk estimates that all of U.S. and EU upstream procurement technology received just $1.5 billion in total funding between 2010 and 2020.

Related Insights

MagicSchool’s AI-Powered Software Is Ushering in the Future of K-12 Teaching

MagicSchool founder Adeel Khan is a former teacher and principal whose AI platform is saving teachers time, fighting burnout, and helping schools build responsible AI experiences for students.

8 min read

Norm Ai Is Using AI to Clean Up the ‘Sludge’ of Regulatory Compliance

John Nay, a founder at the intersection of AI and law, built Norm Ai as a solution to aid compliance officers in highly regulated industries.

6 min read