How Fintech Can Jump on the Generative AI Bandwagon

Generative AI can be a critical ingredient in the way financial services are delivered and make humans 10X more productive. In fact, there are many applications perfect for it.

Opportunities at the Intersection of Fintech and Generative AI, for Founders in Both Spaces

There’s a reason financial services hasn’t been on the top of the list for generative AI companies: generative AI gives the 90% answer and financial services demands 100% accuracy. But it’s a mistake for generative AI to write off fintech, and vice versa. Generative AI can be a critical ingredient in the way financial services are delivered and make humans 10X more productive. In fact, there are many applications perfect for it.

In 2021, fintech was the darling of VC, accounting for $1 of every $5 of venture funding (CB Insights). Then fintech fell from grace in 2022. With inflation surging, the Fed began increasing interest rates in March, changing the fundamental economics under many companies, especially fintech companies whose performance is more directly tied to the cost of capital. Anxiety around the effects of the Durbin Act also rose andregulatory scrutiny increased, kicked off by meme stocks and the Robinhood drama. Putting it together, publicly traded fintech company valuations fell rapidly, some trading even below their cash reserves. According to CB Insights, global fintech funding was down 46% in 2022 compared to 2021. But, the narrative that fintech is dead is way too harsh as fintech still accounted for 18% of all venture dollars invested over the year (TechCrunch).

What has taken the place of fintech on the altar of venture investors? Generative AI. Generative AI as a concept has been around for awhile building off of technologies such as generative adversarial networks (GANs) developed in 2014, transformers in 2017, and Contrastive Language-Image Pre-training (CLIP) in 2021. The technology broke out in 2022 as models became much more performant and cost effective to train and serve, and their output improved considerably. Specifically, machine learning has long been able to outperform humans on perception and optimization tasks, but recent generative AI models have broken through the cognition barrier as well: how to make sense of data and information and understand them in context (Sifted). This has created what many have referred to as the ‘Cambrian Explosion of AI.’ Further, this technology was brought to all of us to play with: Open AI provided free tools for consumers (DALL-E, Chat GPT, etc.) in a short period of time and captured our attention and imagination. While the market is not large today at $8-10 billion, what has captivated investors is the anticipated growth in the market to more than $120B by 2030 (Grand View Research). If you’re interested to learn more about the state of the world of foundation models and AI, check out this great piece by my colleagues on the Infra team here at BCV.

As an investor who spends a lot of time in fintech, one thing that struck me about the coverage of generative AI has been how infrequently applications to financial services are discussed. For example, if you search for a market map of generative AI companies, you’ll see companies that focus on images and art, gaming, text for marketing and sales, and in the dev app space helping developers write code and also those focused on no-code. For example, check out this map from Dealroom or this one from CB Insights. Of course these categories somewhat cover financial services as the industry can still leverage these categories of AI as part of its sales and marketing copy processes or to streamline legal work, just as any company can. But, there seems to be little focus on the way that generative AI can transform the way that financial services products are distributed, underwritten, and serviced within the core financial services value chain. Why is fintech not feeling the love?

By design, financial services companies are conservative

What I will say next will come as no surprise to any student of this industry: most financial services institutions will not be in the early adopters of generative AI writ large. Why? For the same reason as financial services institutions aren’t early adopters of most forms of technology: financial services institutions are conservative by design. The current zeitgeist is that generative AI is amazing and powerful, but it’s anything but accurate and precise, and since financial services has such high accuracy and precision requirements, it’s one of the last places that generative AI should be applied. Let’s explore this more.

As compared to most technology companies, the business model of financial services companies uniquely requires near perfection to avoid high cost outcomes. There is no room for error as financial services is a highly regulated industry where letting a bad apple through an otherwise perfect process can cost an institution their license to operate or ruin an insurer’s entire book of business. That’s game over. So, financial institutions are methodical, conscientious, preferring to (and sometimes required to by regulators) prolong time to value for the customer rather than letting a bad decision through. Important use cases that require 100% accuracy include underwriting, regulatory checks (AML, KYC, BSA/AML, OFAC screening), and accounting / financial reporting.

To illustrate the contrast, if a CRM SaaS company misprices a contract, the company may lose out on gross profit if the cost to serve is higher than expected or the willingness to pay is higher than expected. But, if a commercial insurance company misprices a cyber policy — or even worse underwrites a customer or asset that has risk that is just too high to price — the losses from this one policy could wipe out their entire book.

Back to generative AI, we’ve seen that it works well in processes that need to be “good enough” but not perfect, and financial services institutions won’t compromise on accuracy. So maybe it’s logical for generative AI to pass by financial services? It’s an idea whose time will come to the market, but just not now? Not so fast.

The way generative AI is adopted in financial services won’t look the same as in first generation apps

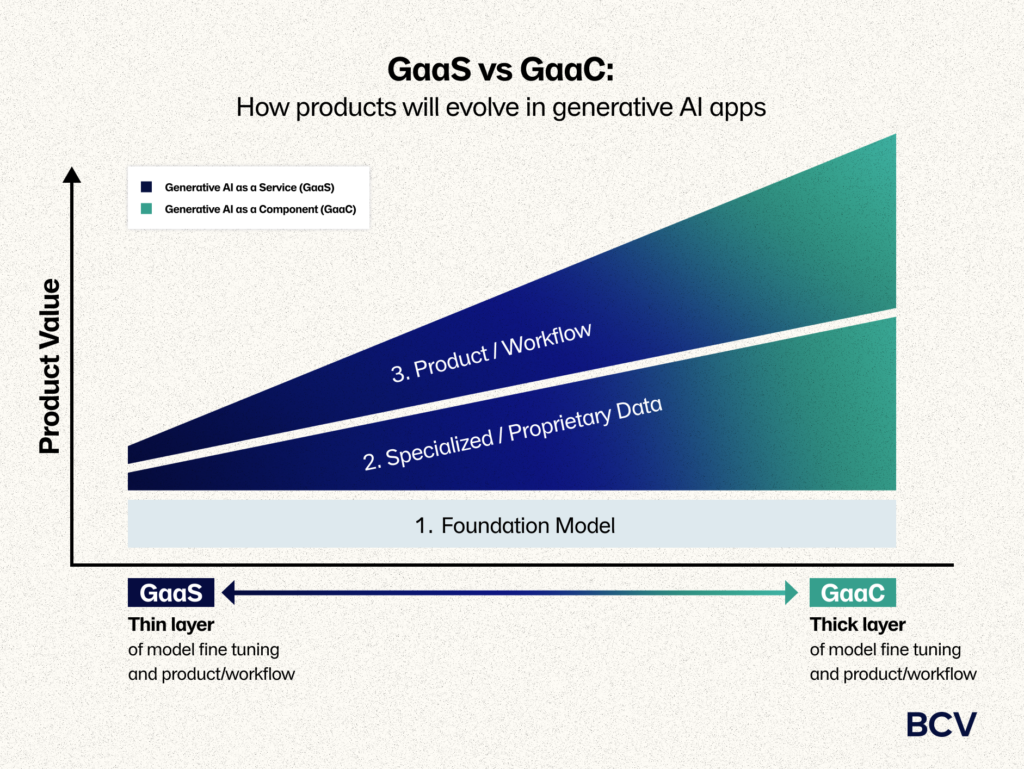

Within the emerging market of end apps built on top of foundation model APIs, the role of AI within the product varies quite a bit. Foundational LLM models are built on top of publicly available internet data, so are very good at tasks ‘out-of-the-box’ that require this generalized knowledge. More specialized outputs require a combination of specialized training data and specialized workflows or product wrappers around the AI. Put simply, all of these apps share the same core components:

API-accessed foundation model;

Fine-tuning of the foundational model with specialized and/or proprietary data (including human interaction with the model so it continues to improve over time); and

Product/workflow to leverage the AI output.

How these apps vary is the relative thickness of the value provided by (2) and (3), where one end of the spectrum — we’ll call GaaS, or generative-AI-as-a-service— has a thin layer of (2) and (3) whereas the other end of the spectrum — we’ll call GaaC, or generative-AI-as-a-component — has a thick layer of (2) and/or (3).

For example on the GaaS side, Jasper uses GPT-3 to write blog posts and create original content for marketing and sales purposes in B2B and B2C contexts. The key value proposition is that the use of generative AI makes the copy automatic, and — while not 100% accurate — it is usually better anyway than copy today. As an example on the GaaC side of the spectrum, Notion recently launched Notion AI, a feature that embeds GPT-3 as a “digital assistant” into the notetaking and project collaboration workflows that Notion offers. Notion is making generative AI a component of their offering that improves the quality of their product.

Many of the first wave of generative AI apps companies that are seeing a lot of hype today are closer to the GaaS side of the spectrum. These companies are common in the first wave because they’re easier to create, relying most significantly on the foundational models. In contrast, it takes more development time to thicken the layer of model fine-tuning and/or wrap-around workflow for product delivery. As GaaS companies continue to mature, we expect they will build more and more intellectual property around their core to differentiate, proving out the ability to effectively use their own data for their specific purpose. The best among them will successfully evolve into GaaC companies (and thrive). In other words, as this market continues to mature, we’re likely to see more and more GaaC companies. The more the generative AI is an ingredient within a software product that solves a hard problem for an end market, the harder it is for the next smart, finely-tuned model to displace the company.

Turning back to financial services, for the foreseeable future, we expect that generative AI apps that successfully sell to financial services companies will be on the GaaC side of the spectrum, delivering AI as a component within the broader software or workflow process. There are two reasons for this. First, financial services data is not part of the publicly available internet datasets that have trained the foundational LLM models; these datasets are proprietary and private. So, apps leveraging the foundational models must fine-tune the models to make them relevant to the financial services use cases. Second, companies in this market will not buy generative AI to do a job because it’s not 100% accurate. Financial services companies will buy software (or services) to do a job, and the best software companies will leverage the best tools to make that job faster, cheaper, and better, including generative AI. In many cases, humans will still need to be in the loop, but the humans will be better informed, more efficient, and produce fewer errors with the assistance of generative AI. We argue that humans verifying vs creating is a huge value add.

And, it turns out, generative AI may be just what the financial services market needs to continue evolving.

Embedding financial services has proven to be stickier than expected

My partner, Matt, has written about the evolution of fintech from discrete to embedded, broadly defined as non-financial services companies offering financial products and services. For example, our portfolio company Trucksmarter is a load board platform designed for truck drivers. Besides offering an app for drivers to manage their business, Trucksmarter has also integrated a factoring product to enable drivers to get paid faster. This is a win-win: it’s better for truck drivers to get more value from one platform and consolidate their business management, and better for the financial institutions that are providing the factoring with more information on the risk.

However, we’re also seeing some inertia in the transition to embedded financial services as the low-hanging fruit has already been picked, so to speak. We’ve seen that the easiest financial products to embed, including payments and wallets / deposit accounts require very little individualized underwriting. For example, any ecommerce website can offer embedded digital consumer payments by leveraging Moov’s API (one of our portcos) within the checkout flow, and doesn’t have to individually underwrite each customer before paying digitally at checkout.

Contrast this to other categories that do require individualized underwriting, for example insurance, where we’ve seen the embedded applications by and large be more restricted to one-size-fits-all products like travel insurance and product warranties. Most individually-underwritten property and casualty (P&C) products, the lionshare of the P&C market, has eluded the embedded distribution model because we’ve seen that embedded distribution often requires a change to the way that the financial services product is manufactured as well. In the case of P&C insurance, it is usually too difficult to manufacture the insurance product (i.e. collect requisite data on the application, underwrite the applicant’s risk, present a quote, select and bind the policy) at a speed required for a delightful embedded customer experience. (Lots to unpack as to why this is, which is the subject of another blog post.)

The other reason we’re seeing some inertia is that incumbent financial services providers have not been sitting ducks; they’ve effectively been able to fight back by (1) matching the digital distribution methods of disruptors (largely enabled by other enabling fintechs), and (2) preserving superior economics through their scale, conservatism, and licensure/regulatory superiority.

Enter the Trojan Horse: Generative AI can help unstick the inertia in financial services innovation

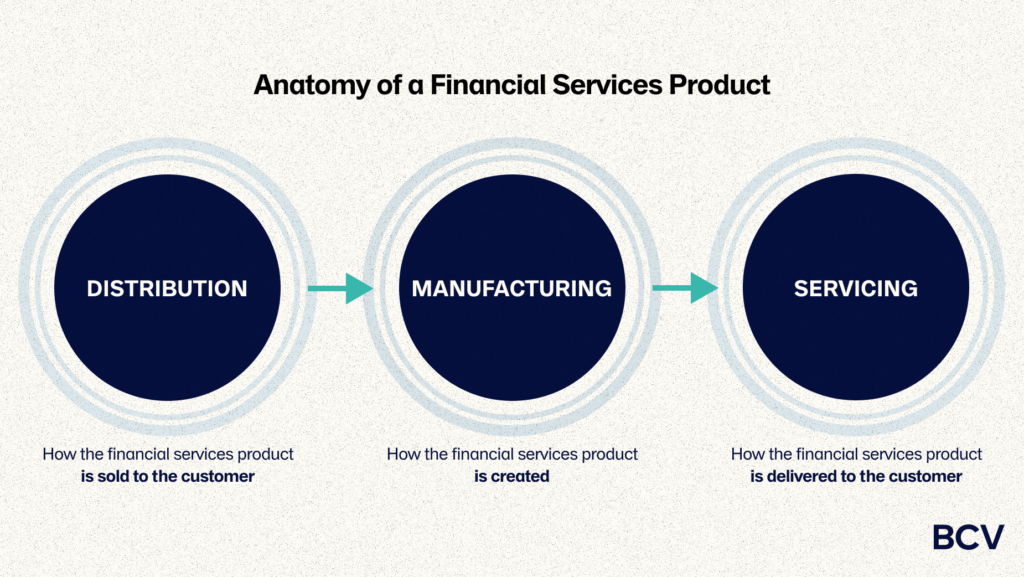

What will it take to unlock the next level of innovation in financial services? Our experience with embedded financial services reveals that the solution must address the friction points in financial services manufacturing, and not just distribution. Generally, financial services products have three stages of the lifecycle:

Distribution: How the financial services product is sold to customers

Manufacturing: How the financial services product is created — once created, a financial services product is a unique instance of a pre-determined product, as agreed to with the relevant regulating authority, for a particular customer

Servicing: How the financial services product is delivered to the customer

How can we innovate on the ways that financial services are delivered? Here’s where I believe generative AI will come in: generative AI is the critical ingredient to make financial services products more accessible and more efficient. When we look at the anatomy of a financial services product, we can see the reality that the complexity in the process comes from the fact that it is a multi-party transaction with varying levels of trust and transparency requiring multiple data sources and multiple modes of interaction. Until recently, AI has by and large not been strong enough, robust enough, or flexible enough to be applied in this complex ecosystem. With generative AI, the innovation frontier has been stretched out and we’re seeing the calculus change.

The next frontier of “embedded fintech” will be embedding generative AI into financial services.

Let’s walk through 10 possible applications of generative AI within the manufacturing of a financial services product. This list is non-exhaustive, and highlights the broad scope of the opportunity. As a bonus, I asked Chat GPT to write one of these descriptions (can you identify which one?).

Distribution Process:

Customized marketing: Generative AI can develop audience-specific messages to market new products or existing product upsells to customers, increasing sales and conversion

For example: Within a consumer banking portal primarily used as a checking account, the bank can accompany an auto-generated personal loan offer with custom messaging based on contextual information about the customer’s identity, spend patterns, and life stage

Document processing: One of the long poles in the tent for applying for many financial services products is the iterative input and verification of information. Generative AI can go even further than verification-based AI to automate the process of extracting information and forward-looking guidance from financial documents, such as from invoices and contracts

For example: When applying for an insurance product, such as a business owner’s policy (BOP), a small business needs to provide some basic information, such as industry, ownership structure, contact information, and business history. This same information is asked in different ways on all applications. Generative AI can ingest the information from one application and splice it to input it into other applications, so the broker or small business owner only needs to input information once to receive quotes from multiple carriers

For example: Accounts Payable solutions collect and organize the payments that a company makes to suppliers and vendors. These solutions reconcile invoices against payments and add valuable meta-data to correctly categorize expenses within financial reporting. Generative AI provides stronger capabilities to accurately generalize and label expenses

Information validation: The application process for financial services often requires validating information. The most difficult products to validate include those that can be represented in multiple formats rendering simple rules-based logic useless. Rather than have humans manually check policies, or code policies based on contents so rules-based logic can work, generative AI can determine whether a policy meets standard criteria

For example: A driver applying to a rideshare program submits their car insurance policy. The rideshare program can automatically review the policy-level information associated with this policy to see if it meets the standards of their program (or not)

Manufacturing Process:

Fraud identification: Generative AI can produce new training data to train and re-train fraud models. One of the challenges with piracy and fraud has been the cat and mouse game of security providers building to address the latest exploited weakness, only for fraudsters to find the next weakness. Training models on yet-unseen examples of fraud generated by generative AI provides the opportunity to stay one step ahead

Memo writing: Believe it or not, many financial services products still require a formal memo be submitted and reviewed by committee for major decisions. Similar to the opportunity to apply generative AI in the legal world, generative AI can review a full application and write a first draft of a memo

For example: Loan officers for mortgages above a certain level prepare memos to present the underwriting case to committee. Generative AI can expedite this process by providing (a pretty good) first draft

Risk identification and portfolio construction: Generative AI can help companies consider all available data to more accurately forecast future performance and identify uncorrelated risks

For example: Generative AI can help the FP&A team within a company consider the full body of data to better forecast the future sales and profitability of a company — from individual sales plan based on pipeline and AE sentiment from internal communications to past performance and reporting bias to the costs of different departments, including planning headcount and budgeting

For example: Lending and insurance companies need to scan for trends in their portfolios by industry, geography, credit quality, business size/stage, etc. Analysts are looking to avoid density mistakes of the past, and identify new risk areas before they become problems. Generative AI can substantially automate the work of several risk analysts who generate regular reports for the internal credit and board risk committees

Pricing and fee optimization: While many financial services products require pretty homogeneous pricing (or at least pricing consistent with rules submitted to the regulators), some products can vary widely within regulated bands. Using generative AI, financial services organizations can better evaluate the willingness to pay for certain products or ability to pay certain fees and maximize customer LTV

Product selection: Financial services products are often difficult to understand and not described in layman’s terms, which leads to significant deterioration in conversion percentage and speed. Using generative AI, financial services companies can explain the product offering to customer prospects, or compare different financial products, as well as answer follow-up questions around coverages or limits

For example: Generative AI can be used by a commercial broker to describe in words what an insurance policy covers, compare coverages from different quotes, and respond to questions from the applicant about coverage

Servicing Process:

Automated relationship management: Relationship managers support clients to get the most value out of their product, such as insurance brokers, private wealth managers, and commercial bankers. The highest NPS relationships are highly customized and responsive, but this is too expensive to make available to any customers but the highest value customers. With generative AI, sensitive, custom service can become standard

For example: Generative AI can support wealth managers to manage financial plans for their customers. Generative AI can help interpret risk appetite, identify fears, and pick up on sentiment shifts. This is critical to help customers “hold” when appropriate and “sell” when necessary

Customer service: AI-powered chatbots can help companies provide 24/7 customer service and support, handling a wide range of customer queries and issues, such as providing financial advice and helping with account management

Who stands to flourish in the “New World”?

There are a few players that are well-positioned to take advantage of generative AI in the financial services world:

Incumbent financial services institutions: As described above, generative AI requires a foundation model (e.g. OpenAI’s GPT-3), plus context-specific training data to fine tune the underlying model to a specific use case. Generally, the more data, the better, which puts incumbents with data supremacy (both in terms of duration and depth) in an advantaged position. Of course incumbents will need to be able to reliably access the data, and have the organizational will to take advantage of the data.

Nimble enablers who can partner with incumbents: Incumbents may be best able to take advantage of their data by partnering with enablers who have the specialized knowledge to make use of the data and don’t face the same institutional conservatism as many incumbent financial services organizations.

Disruptors who can own the full value chain: Given the primacy of data, incumbents have an advantage, but there are multiple dimensions to data. Disruptors can accrue horizontal data (one space or application across many companies), vertical data (one company across many spaces or applications), or usability data (process data on how information is used). Further, disruptors that can develop their own data by focusing on financial services workflows, enabling them to prospectively build a superior product experience vs the incumbents.Disruptors are especially well-positioned as the market evolves toward GaaC since they typically have faster product velocity to find and maintain product differentiation.

Calling all generative AI founders to fintech, and fintech founders to generative AI

One possible critique of the list above of generative AI applications within financial services is that none of the examples above are revolutionary; rather, each is an opportunity to incrementally improve the process of providing financial services. This is a feature, not a bug! What we find so exciting in imagining the future applications of generative AI within fintech is that the layering of multiple of these incremental improvements can revolutionize the value we can capture from financial services products. Another way to think about it: if today’s generative AI can get to 90% accuracy and a human review can get to 100%, you are making a human 10X more productive and hitting the accuracy threshold required to deliver financial services.

A few pointers for early builders in this market:

Get to measurable ROI quickly: The value of a new app must more than make up for the cost of changing technology or process. Financial services organizations are creatures of habit, so the value proposition must be so significant that adoption is a no-brainer. We expect apps that can show ROI within test environments to be particularly impactful.

Don’t steer away from critical or high stakes workflows, focus here: This may be counterintuitive, but don’t be afraid to be laser-focused on the highest stakes part of the workflows for financial services organizations. They can’t afford to get these wrong, and are willing to spend disproportionately to make sure that a bad decision doesn’t go through. These areas also have a higher attention from the senior team, which is often required to push through innovative technology.

Be thoughtful about data rights: As mentioned, there’s a high value of data in this market because so little of financial services data is public. The companies that are set up to succeed are those who have access to the most and highest quality data to fine-tune the foundational models. Data access can be inherited, accumulated, or purchased. Companies building in this space should strategically consider ways to maximize the surface area of their data, recognizing that there will sometimes be the need to sacrifice depth for breadth (e.g. de-identified data from all customers).

Build a thick enough software stack that you can be transparent around your models while not giving up the keys to the kingdom: AI models can be difficult to understand, interpret, or replicate, which can make it difficult for companies to explain how decisions are being made. This lack of transparency can also make it difficult for regulators to ensure that AI systems are being used in an ethical and fair manners. If a regulator does not understand or agree with a process used by a fintech, they can shut the fintech down. This is particularly fraught topic in financial services since AI models trained on biased data can lead to discriminatory or unfair decisions. Regulatory bodies are particularly attuned to the threat of analytics exacerbating existing biases in the founders. Builders in this space shouldn’t expect models to be maintained as “trade secrets,” but should have robust enough product and workflow IP so that sharing the models with regulators doesn’t upset a company’s strategy.

We’re early in this journey and are excited to see this market unfold over the coming years. If you are building in this space or considering how to take advantage of generative AI within your fintech platform, we’d love to hear from you.

Special thanks to many who contributed to and pushed my thinking for this piece, including Annie Robertson Hockey, Animish Sivaramakrishnan, Erin Yang, Jill Greenberg Chase, Natalie Vais, Niko Bonatsos, Zach Smith, and my partners Christina Melas-Kyriazi, Dawit Heck, Matt Harris, Noah Breslow, Rak Garg, Sam Crowder, and Slater Stich.

We’re at the scary part of “the hero’s journey” in fintech, with a bottom for funding and a BaaS crisis, but we’re about to enter a new, exciting stage.